FIRE Calculator Guide: How to Calculate Financial Independence and Retire Early

For a good while, Sunday evenings used to leave me a little blue.

Tomorrow it would all start over again — five more days of the same dull grind.

I'd end up staying up too late without meaning to,

and when Monday's alarm went off,

I'd be packed into a crowded train, racing to clock in on time.

Is this really the life I want for the next 30 years — maybe even longer?

If you're anything like me and have grown tired of the endless overtime and workplace pressure, the FIRE movement that's swept the world in recent years is worth a real look. To me it isn't just another money strategy — it's a quiet revolution about taking back control of your own life. I've built a 👉 Retirement Calculator right into this article, so give it three minutes and let's get to FIRE together.

What Is FIRE — Financial Independence, Retire Early?

FIRE stands for Financial Independence, Retire Early. Through a high savings rate and long-term investing, you accumulate enough assets so that passive income fully covers living expenses — achieving financial freedom at any age, not just 65.

The core formula: Annual Expenses × 25 = FIRE Number. This comes from the 4% safe withdrawal rule established in the 1998 Trinity Study by Cooley, Hubbard & Walz — historically, withdrawing 4% annually from a diversified portfolio has a 90–95% success rate over 30 years.

Example: Annual living costs of $40,000 → FIRE number is $1,000,000.

The 3 Golden Steps of FIRE

Achieving financial freedom isn't just about budgeting and saving (though that matters a lot)

It's about first understanding your own needs

Setting clear goals

Then reaching them through a systematic strategy:

Step 1: Calculate Your FIRE Number (The 25x Rule)

This is FIRE's most classic starting point, rooted in the famous 4% Rule (from the Trinity Study)

Once you accumulate assets equal to "annual living expenses × 25,"

And invest in a solid portfolio (like global equity ETFs)

Withdrawing 4% per year (adjusted for inflation),

The historical probability of running out of money within 30 years is between 5–10%

Formula: Annual Expenses × 25 = FIRE Target

Example: Annual living costs of $24,000 → FIRE number is $600,000.

Step 2: Review Spending and Dramatically Boost Your Savings Rate

The average person saves 10–20%

But many FIRE practitioners push that to 50% or more

The goal is to reach financial independence as early as possible

Cut non-essential spending (frequent car upgrades, luxury goods)

Distinguish between "wants" and "needs"

Redirect what you save into investments

Step 3: Build a Robust Passive Income System

After these past few years, most of us feel it acutely

Money sitting in a bank account just gets eaten away by inflation

So we must invest to make money work for us

Common allocations include low-cost global index ETFs, high-dividend stocks, or rental income from real estate

Of course, any side-hustle income (cash flow outside of investments) is the cherry on top

What's Your FIRE Number? Calculate It Now

Gut-feeling finance is easy to get lost in

Data is what tells you whether you're actually on the right track

Allow me to shamelessly plug this handy little tool: 👉 Retirement Calculator

Enter your age, current savings, and expected expenses

Enter your age, current savings, and expected expenses

It quickly simulates how far you are from financial freedom

And runs historical bear-market stress tests

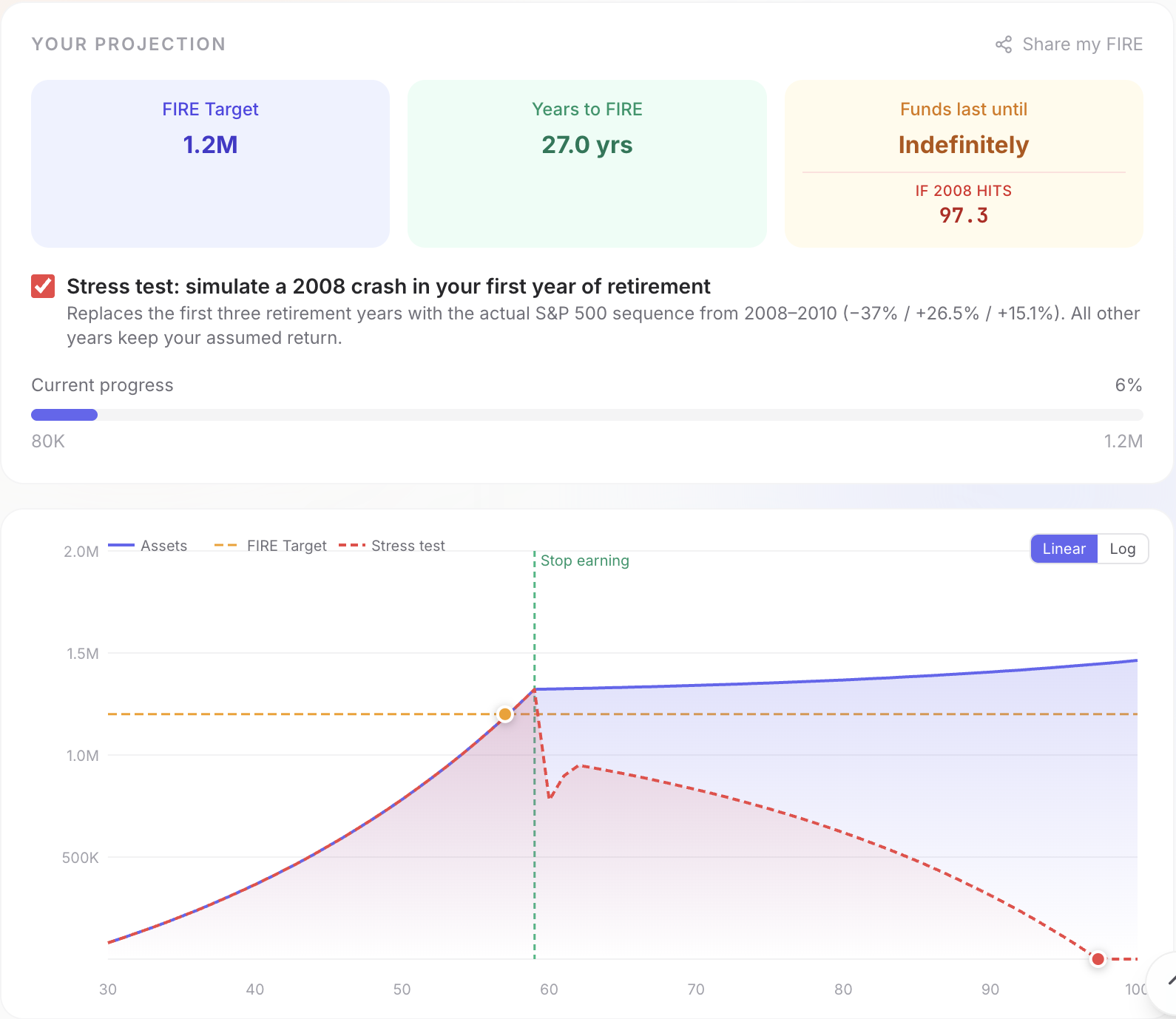

Is FIRE Safe? The Importance of Bear-Market Stress Testing

The Trinity Study shows the 4% Rule has a very high success rate over a 30-year retirement

But what if you retire early (potentially needing 40–50 years) or hit an extreme bear market?

That's exactly why I built a stress-testing feature

By simulating historical data,

You can see performance under extreme scenarios

And adjust your financial strategy in advance (e.g., reducing spending during a bear market)

Find the FIRE Flavor That Fits You

After FIRE took hold, different branches emerged

Here are the common varieties

Choose based on your risk tolerance and lifestyle:

- Lean FIRE: Aggressively cut expenses and retire early on a smaller nest egg.

- Fat FIRE: Maintain or improve your quality of life, requiring a larger asset base.

- Barista FIRE: Once you've saved most of your retirement fund, shift to easy part-time work to cover current expenses and let your assets keep growing.

- Coast FIRE: Work hard to save a seed amount when young, then "let it ride" through compound interest. You only need to earn enough to cover current living expenses.

I believe retirement doesn't have to mean doing nothing

It means finally being able to "only do what you want to do"

Without having to bow and scrape for a paycheck

Use FIRE as Your FU Money

Personally, I lean toward Barista FIRE or Coast FIRE

Because they give you "work optionality" rather than forcing you to stop working entirely

And they provide better flexibility across various market conditions

Even with traditional FIRE,

Simply moderating your spending in bear-market years

Can dramatically reduce the risk of running out of money early

FIRE is a systematic approach

That helps people reclaim agency over their work and lives

But the volatility in between requires financial intelligence and adaptability

I used to feel like retirement was impossibly far away

But after actually running the numbers,

I discovered there are many different ways to accelerate my retirement plan

I hope this article and tool can help you too

Let's become people who control their own lives. 😎

This article is for financial education purposes only. All investments carry risk. All data and simulations are based on historical back-testing and do not represent future performance. Please make decisions based on your personal financial situation, risk tolerance, and advice from a professional consultant.

References & Further Reading

Frequently asked questions

What is FIRE — Financial Independence, Retire Early?

FIRE stands for Financial Independence, Retire Early. The core idea: through a high savings rate and long-term investing, accumulate enough assets so that passive income fully covers living expenses. Once your portfolio reaches Annual Expenses × 25 (the FIRE number), you can theoretically retire at any age.

What is the 4% Rule?

The 4% Rule comes from the 1998 Trinity Study (Cooley, Hubbard & Walz). It states that a retiree who withdraws 4% of their portfolio annually, adjusted for inflation, has historically had a 90–95% chance of their portfolio lasting 30 years. The FIRE number of 25× annual expenses is derived directly from this rule (1 ÷ 0.04 = 25).

What is a FIRE number?

Your FIRE number is the portfolio size at which you can safely withdraw enough to cover all living expenses indefinitely. The classic formula: Annual Expenses × 25 = FIRE Target. Example: $40,000/year in expenses → FIRE number of $1,000,000.

What are the different types of FIRE?

Lean FIRE: retire early on a small nest egg by aggressively minimizing expenses. Fat FIRE: maintain or improve quality of life, requiring a larger asset base. Barista FIRE: save most of your retirement fund, then shift to part-time work to cover current expenses while assets keep growing. Coast FIRE: save enough early that compound interest alone will grow it to your FIRE number by traditional retirement age.

Is FIRE safe during a market downturn?

Sequence-of-returns risk is the main danger — retiring right before a major market crash while withdrawing from a falling portfolio. The AppicLab FIRE calculator includes a 2008-scenario stress test to show portfolio survival under the worst historical drawdown in modern memory. Moderating spending in bear-market years significantly reduces this risk.

About the Author

indigo.la.ringo

A software engineer chasing the slash-career dream. Was trying to figure out my relationship with the world — now being forced to figure out my relationship with AI. Lately, obsessed with figuring out the relationship between people and money. Either way, whatever answer I land on, it's fine.

Feedback

Thoughts or suggestions after reading? I'd love to hear them.