Should Young People Lever Up Early? A Look at Lifecycle Investing

I recently finished Lifecycle Investing

written by two professors from Yale

Building on the investment ideas of Nobel laureate Paul Samuelson

they propose a practical investing method

that, holding risk constant

can lift your returns by more than 50%

How exactly does a free lunch like that work?

Come take a look with me

What lifecycle investing actually says

Lifecycle Investing

is the work of professors Ian Ayres and Barry Nalebuff

My own translation of the whole book boils down to one sentence

Diversify your risk across time

Here's an example

We all know about sequence-of-returns risk

If we run into a black swan right at retirement

we may have to cut our withdrawal amount

and our quality of life in retirement takes a big hit

But if we had enough capital

couldn't we ride out that temporary crash-driven dip?

If we believe the stock market goes up in the long run

doesn't that mean every pullback is temporary?

Thinking about it that way

the solution is simple

just wait a few more years

So how do we buy ourselves those extra years?

We can move future money into the market earlier

so every dollar spends more time running in the market

Time diversification: spreading risk across a lifetime

We all know not to put our eggs in one basket

so we might buy an ETF

or even invest in the whole world

But the traditional approach can't diversify risk across time

The whole point of lifecycle investing is to raise your exposure when young

and lower it as you age

It's like taking some of your old-age capital and investing it earlier

Even if it takes a hit

because it entered the market earlier

it also gets to recover earlier

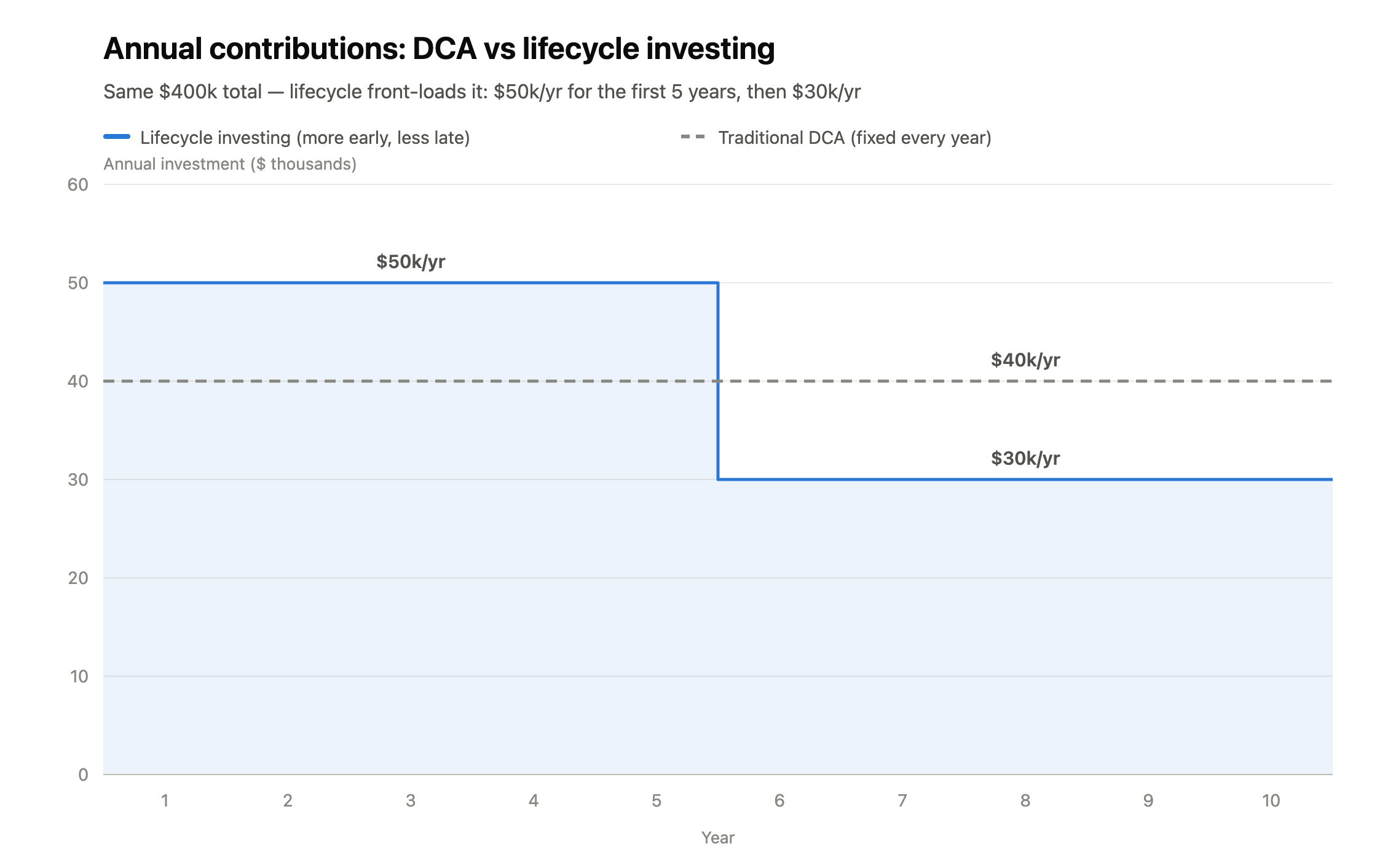

In practice it looks something like this

Say the total amount we'll put into stocks is $400,000

invested over ten years

Traditional DCA might be $40,000 per year

Lifecycle investing would instead suggest

front-loading more — say $50,000 a year early on

and dropping to $30,000 a year when we're older

The total invested is exactly the same

but the money gets into the market sooner

more of your capital enjoys the market's growth

and it has more time to recover from downturns

I made a quick diagram:

The authors suggest going up to 2x leverage when young

that is, letting twice the capital participate in the market

then gradually stepping down to 1x in between

I'll spare you the details here

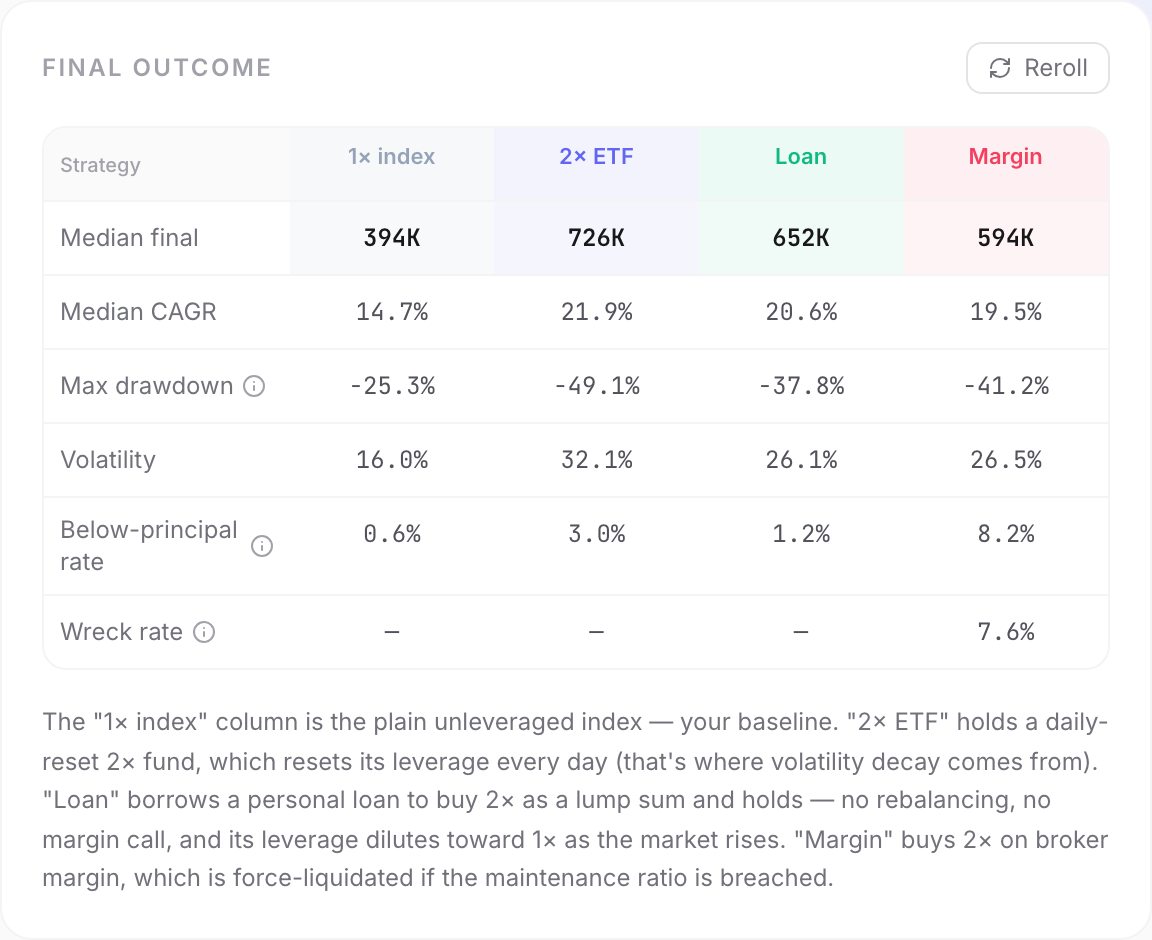

With this approach

in their historical backtests

at the same level of risk

the median outcome improved by a remarkable 50%

In practice, how do you get more than 1x exposure?

Simply put

you borrow to move future income into the market earlier

There are just different ways of borrowing to get invested

such as:

- Leveraged ETFs

- Loans

- Futures

- Options

- Margin trading

Let's go through these methods and the practical details one by one

Loans

The simplest way is a personal loan or a mortgage top-up

to borrow extra money and put it into the market

But the interest rate varies from person to person

so if your rate is too high

the math may not actually work out

You can start with this Loan-to-Invest Calculator

to see whether the loan is worth the risk

Buying on margin

In the Taiwanese stock market

you can buy stocks through a margin account

The current rule puts the initial margin at roughly 40%

meaning you can buy $100,000 of stock with $40,000 down

which also means you've opened 2.5x leverage on that position

Put up $50,000 instead

and you're back to 2x

But brokers aren't charities

margin interest rates are actually quite high (around 4–6%)

And Taiwan has a maintenance ratio requirement (currently 130%)

Say you buy $100,000 of stock with $50,000 down

when your stock's market value falls to $65,000

your maintenance ratio sits exactly at 130%

At that point the broker demands more cash to restore the ratio

or you get forcibly liquidated — a margin call

Futures

Futures work a lot like a margin system

You put down a deposit as collateral

but when your position's value drops close to overtaking your margin

the futures broker demands more collateral or force-closes you

That's why so many people open oversized leverage and lose everything

The other risk with futures is that you must roll before expiry

that is, roll this month's contract into next month's (unless you want to exit the market)

which means slippage and rollover risk and cost to account for

Options

An option, simply put, is buying the right to buy or sell an underlying asset

but this is far too advanced for a beginner like me

Even though the book itself recommends this approach

the Taiwanese and US markets are quite different

so I haven't dug any deeper into this part myself

Leveraged ETFs

A leveraged ETF is a fund that uses derivatives (futures, swap contracts)

to track an index and amplify its daily return by a multiple (usually 2x or 3x)

Simply put, you pay a fund manager to handle the derivatives

and they work to deliver:

the index rises 5%, I rise 10%

and vice versa

The upside is you don't have to manage anything yourself (you've outsourced it)

But besides the higher expense ratio leveraged ETFs charge

there's also volatility decay

You can use this Leveraged ETF Calculator

to get a feel for what volatility gives and takes

So which one is best?

Everyone gets different financing terms

and wants to invest in different things

That's why I built this 2x ETF vs Loan vs Margin tool

so you can see which set of terms suits you best

Plug in your own assumptions

gauge your own risk tolerance

and see whether the lifecycle-investing strategy is right for you

Comparing the methods

I believe everything that exists has its reason

Even if some strategy has a spectacular return

whether you can actually hold on to it is another question

There's no single best answer

only the one that fits you

Here's my rough summary of pros and cons:

- Loan: the interest rate is gravity — you need solid proof of income or assets to negotiate a low rate

- 2x ETF: set-and-forget, but you pay the expense ratio; the rallies feel great, but you must stomach volatility decay in sideways markets and a halved account in drawdowns

- Margin: when the maintenance ratio gets low you must be able to inject cash, and the rate is usually on the high side

- Futures/Options: advanced derivatives — I have limited experience with them myself

Closing thoughts

People have always said "never borrow to invest"

but I think that mindset is starting to shift

Think about it — real estate is one giant leveraged loan investment

You may only need a 20% down payment to buy

which means you've opened 5x leverage from day one

yet nobody criticizes homebuyers for it

What lifecycle investing left me with most is this:

"Time" is a young person's greatest asset.

That's also why I believe long-term investing

is how ordinary people climb the ladder

May we all make it to the next stage

This calculator and this article are for educational purposes only and are not investment advice. Lifecycle investing is a long-term framework that demands discipline and preconditions; leverage magnifies both gains and losses, and real margin trading has intraday maintenance calls that can liquidate you faster and deeper than any model. Consult a qualified financial advisor and never invest more than you can afford.

References and further reading

- Ayres & Nalebuff — Lifecycle Investing (official site)

- Lifecycle Investing — Traditional Chinese edition ebook (Kobo)

- SEC — Investor alert on leveraged and inverse ETFs

- Investopedia — Leverage: definition and risks

- The Shell Seeker — Lifecycle Investing book notes (Medium, Traditional Chinese)

- AppicLab — Borrowing to Invest: Reckless Gamble or Rational Choice?

- AppicLab — Lump Sum or Dollar-Cost Averaging? Use the Risk Report to See Your Real Odds

- AppicLab — FIRE Calculator Guide: How to Calculate Financial Independence and Retire Early

Frequently asked questions

What is lifecycle investing?

It was proposed by Yale professors Ian Ayres and Barry Nalebuff in their book Lifecycle Investing. The core idea: your investment exposure shouldn't be based only on 'how much money you have right now,' but on 'the total amount you'll invest in the market over a lifetime.' When you're young your capital is small — even 100% in stocks is a tiny share of your lifetime wealth, which means your risk is over-concentrated in the second half of your life. They argue that moderate leverage when young (capped around 2x) pulls your equity exposure forward and spreads it evenly across more years, reducing the time-concentration risk of 'all your chips riding on just a few years.'

Why does lifecycle investing cap leverage at 2x rather than higher?

The authors explicitly set the leverage ceiling at 2:1, and dial it down gradually as you age and your assets grow. The reason: leverage magnifies long-term expected returns, but it also magnifies drawdowns and the risk of ruin. Beyond 2x, a single deep crash can wash you out of the market entirely — destroying the very premise of 'staying invested for the long run.' Two-to-one is the compromise between 'spreading time risk' and 'still surviving a crash.'

For 2x exposure, should I pick a 2x ETF, a loan, or margin?

All three give you roughly 2x the index's daily moves, but the mechanics are worlds apart. A 2x ETF resets its leverage back to 2x every day — the leverage is locked in, but you pay an expense ratio and volatility decay erodes you in choppy markets. A personal loan is a one-time borrow-and-hold: it dodges the daily decay and can never be margin-called, but the leverage dilutes toward 1x as the market rises, and you must keep repaying the debt throughout. Broker margin is the cheapest, but your shares are the collateral — fall below the maintenance threshold (commonly 130% in Taiwan) and you get force-liquidated.

Why does margin get liquidated in a crash while a loan can ride it out?

Because a personal loan has no claim on your position — the lender only cares that you make your monthly payments, not what the stock price does. When the index drops 35%, a 2x margin position falls below the 130% maintenance ratio and the broker sells you out at the bottom, locking in the loss and making you miss the rebound. With the same drop, a loan-funded holder is underwater on paper but still holding — when the market comes back, so do they. That ability to 'hold on' is exactly what lifecycle investing depends on.

Is lifecycle investing for everyone?

No. It has strict prerequisites: you need stable, predictable future income (your salary is your 'bond-like' allocation), the stomach to watch your account get cut in half without selling at the bottom, and you must do it entirely with money your life doesn't depend on. If your income is unstable, your emergency fund is thin, or paper losses keep you up at night, leverage will only sweep you out of the market faster. It's a long-term framework that demands discipline — not a shortcut to getting rich.

About the Author

indigo.la.ringo

A software engineer chasing the slash-career dream. Was trying to figure out my relationship with the world — now being forced to figure out my relationship with AI. Lately, obsessed with figuring out the relationship between people and money. Either way, whatever answer I land on, it's fine.

Feedback

Thoughts or suggestions after reading? I'd love to hear them.