Lump Sum or Dollar-Cost Averaging? Use the Risk Report to See Your Real Odds

While researching borrowing to invest

to convince myself to hold on with more conviction

I ran a lot of risk simulations

hoping to be ready to face the worst case

and ended up with a few new realizations instead

You've probably heard people tell you to buy half first

and to just hold once you've bought in

But is there any basis to these sayings?

Let's find out together

The investment risk report

I added a new feature to the 👉 loan-to-invest calculator:

you can simulate different market environments

but if you simply set the loan rate to 0

you can treat it as a lump sum you have on hand right now

about to enter the stock market

turning it into a plain comparison of lump sum vs. dollar-cost averaging

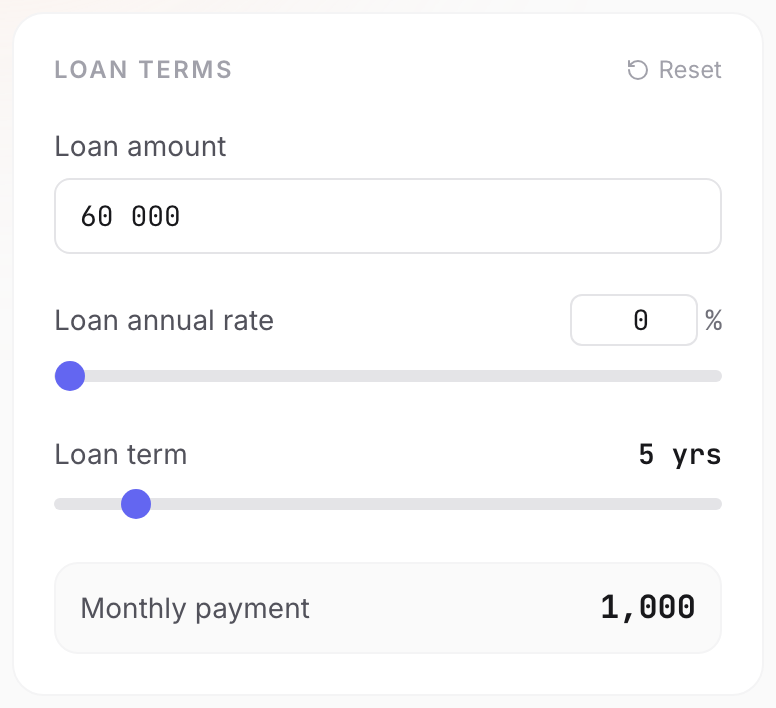

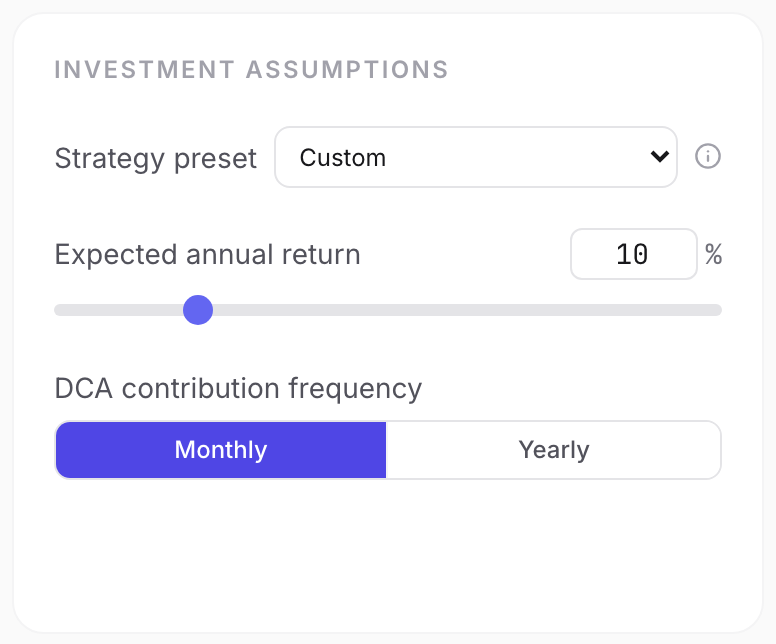

Assuming a total of $60,000 invested vs. $1,000 a month

with the loan rate set to 0 (swap in whatever number you like)

and a broad stock index over the past ~20 years (2006–2025) as the input

- CAGR (compound annual growth rate) 10% ( these recent years ran hot, so I dialed it down a bit )

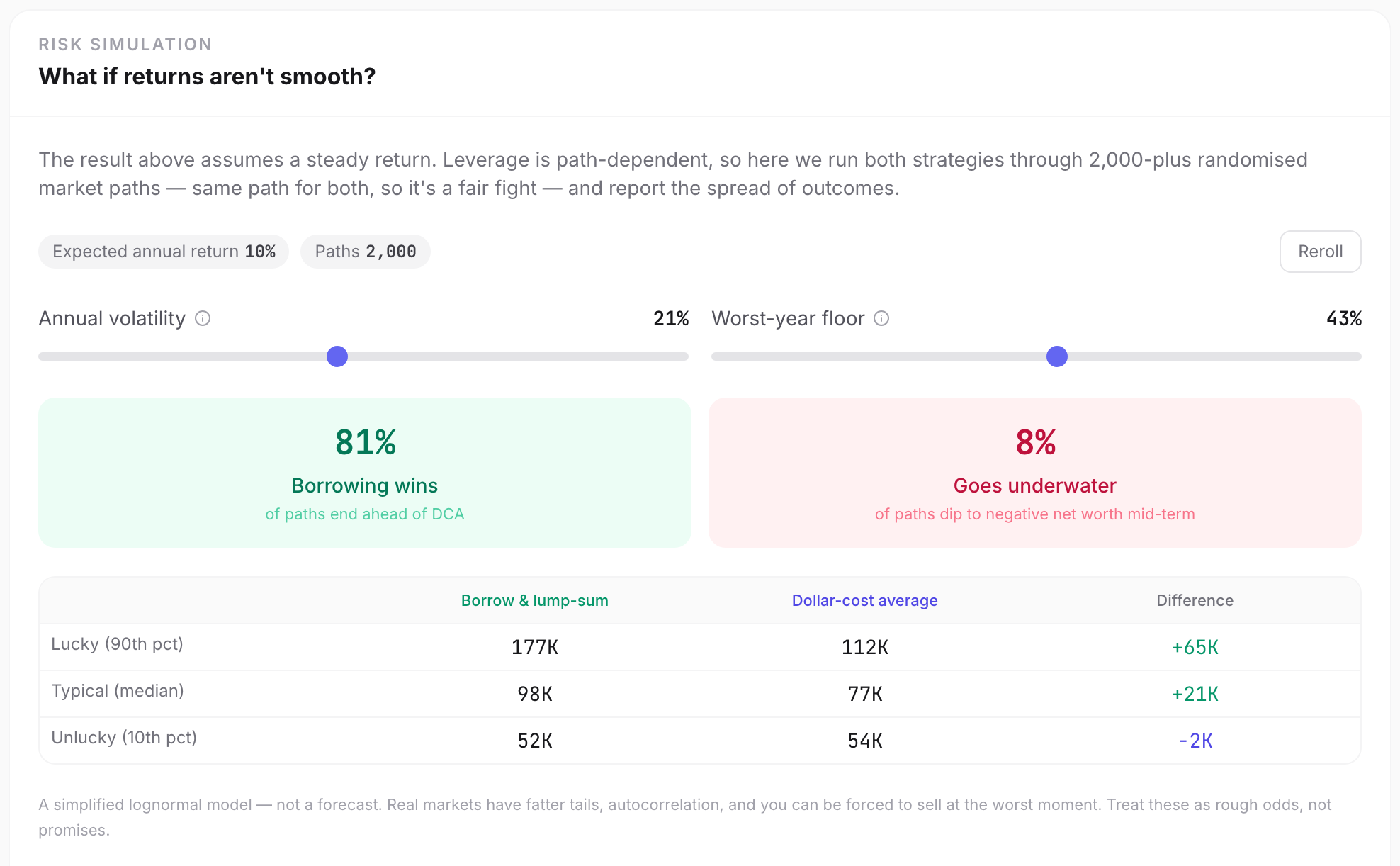

- annualized volatility around 21%

- worst single-year drop 43% (financial crisis)

Through the Monte Carlo simulation below you'll find that

over a 5-year horizon

the lump sum wins about 80% of the time (this is at zero borrowing cost; interest would lower it)

even knowing the odds are this good

why can't we bring ourselves to buy?

The path we never see

After all, humans are emotional creatures

Scholars have proposed various theories to explain this

prospect theory, for instance, says we may overweight the odds of extreme events

and loss aversion adds its own braking effect

so that even with cash in hand

we don't dare go all in

Even when we rationally know the odds are better

we can't see all fourteen million possible futures the way Doctor Strange could

So what can we do?

Run the worst-case script first

If you read my previous post on borrowing to invest you'll remember

the thing a lump sum fears most is a crash in the very first year

which is exactly why I added the simulation report feature

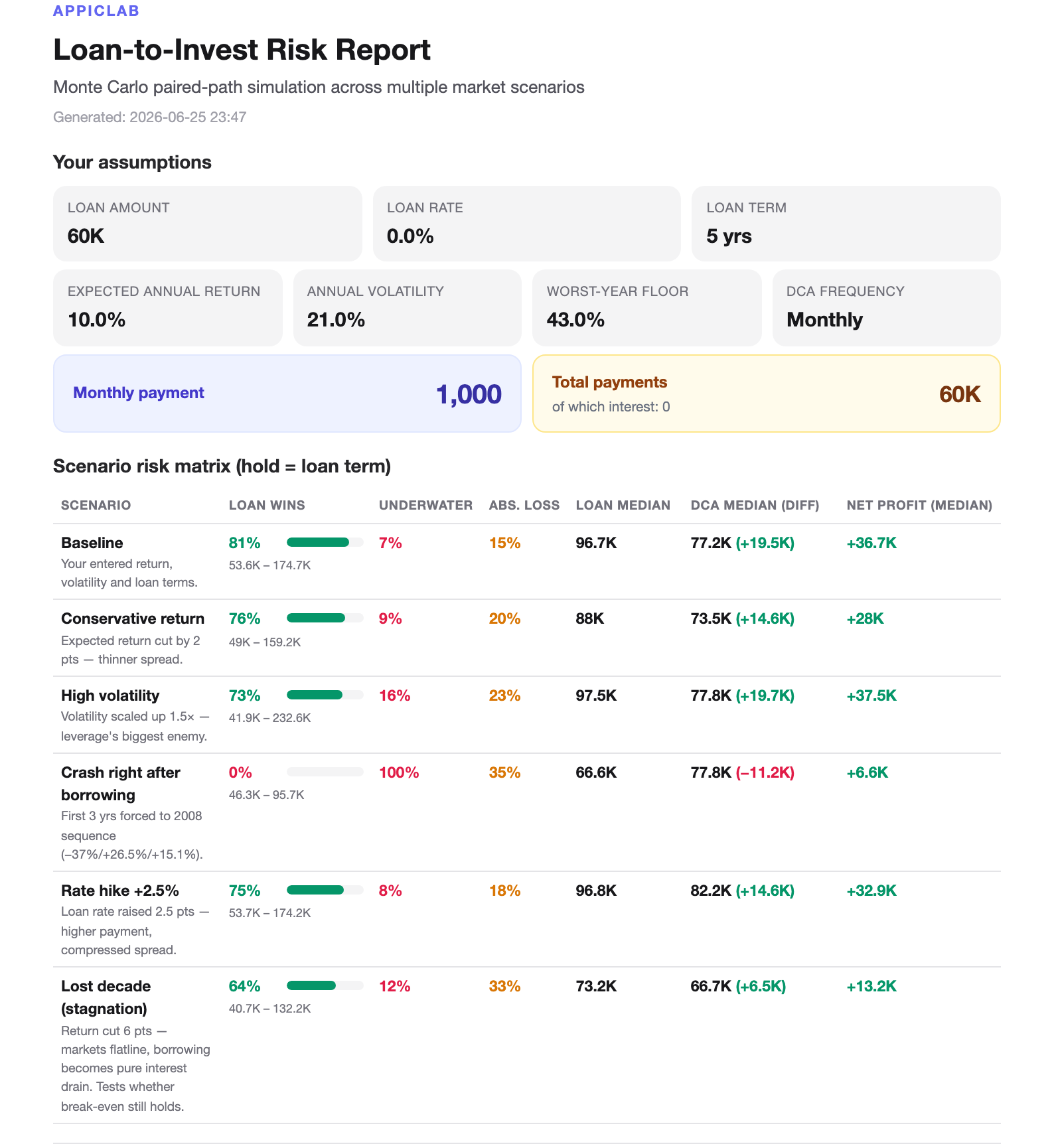

click "generate report" below to analyze your outcomes across different scenarios

We'll again assume a total of $60,000 invested

- lump sum vs. $1,000 a month (1,000 × 12 × 5)

- loan rate set to 0

- CAGR (compound annual growth rate) 10%

- annualized volatility around 21%

- worst single-year drop 43% (financial crisis)

The report shows that

the lump sum wins basically everywhere else

except when a crash hits in the first year

which is exactly sequence-of-returns risk

Is there any way to avoid this risk?

Plenty of seasoned investors say: if you're scared, buy half first

and while building this simulation I stumbled onto something

buying half may not be an old wives' tale after all

but a kind of hard-won rule of thumb

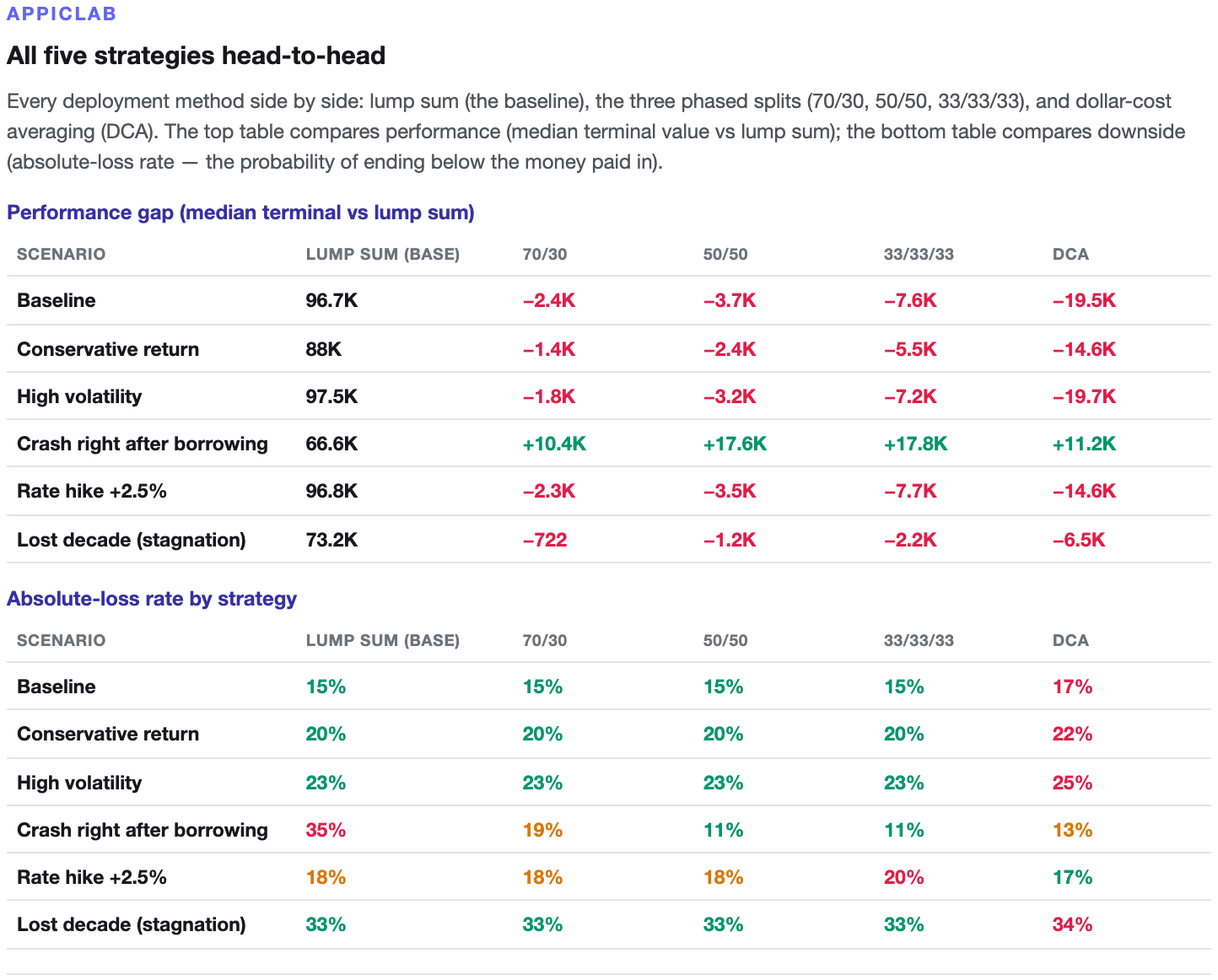

On the risk-assessment page I lay out several different strategies

basically comparing buying half, splitting into three, and so on

and you can see that buying half dramatically lifts the win rate when a crash hits in year one

while the performance barely differs

Put plainly, this is a form of timing the market

We can't predict when a crash will come

nor how long a bear market will last

but if you use half of one year's gains as insurance

so you can buy in with peace of mind

why not?

After all, markets are mostly long bulls and short bears

and only by surviving pullback after pullback

do you reach financial freedom

The long game is the real finisher

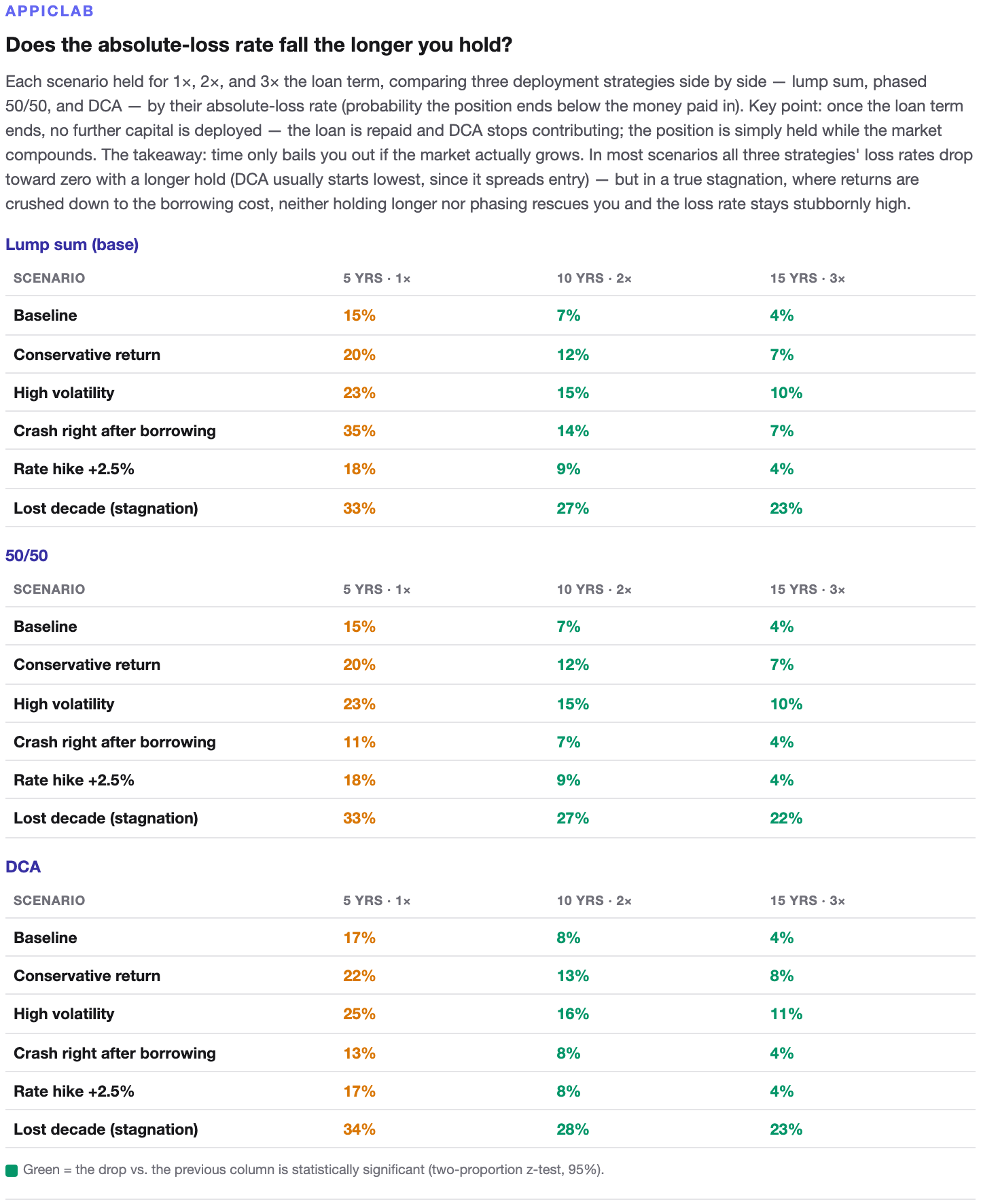

You've probably noticed that over the 5-year simulation

there's roughly a 20–30% chance

of ending up in the red

So is there another move?

Let's look at the next page

You'll find that if we stretch the timeline

the loss rate falls

out to 15 years

it drops into the single digits

and even in the most hopeless stagnation scenario

the loss rate keeps falling

Maybe time really is the one and only answer

and it makes me believe more and more

that getting rich is genuinely simple

but you need patience

a great, great deal of patience

Closing thoughts

This piece is something I'm leaving for my future self

so that if the day comes when a Financial Crisis 2.0 really does hit

I'll remember Water Breathing, Eleventh Form

— Dead Calm —

This tool and article are for educational reference only. Monte Carlo simulation estimates probabilities by random sampling — it is not a prediction of the future. Borrowing to invest is leverage, which magnifies both gains and losses; consult a qualified financial advisor and act within your means.

Further reading

Frequently asked questions

Lump sum (LSI) vs. dollar-cost averaging (DCA) — which is actually better?

Both strategies put the exact same cash out of your pocket each month; the only difference is whether the money enters the market early. Over the long run, as long as your investment return stays comfortably above your borrowing cost, the lump sum has the higher expected value — at 10% return, 21% volatility, over a 5-year horizon, the lump sum wins in roughly 80%+ of paths. But "wins on average" isn't "wins every time," and the biggest variable is sequence-of-returns risk.

What is sequence-of-returns risk, and why is it so dangerous when you've borrowed?

It means the order in which returns arrive heavily shapes the outcome, even when the long-run average is identical. Borrowed money is fully invested on day one, so a big drop in the first year or two hits your largest principal immediately — far worse than the same crash ten years later. That's why the report includes a "crash in the first year" scenario that drops a financial-crisis-sized fall right onto your entry year as a stress test.

People say "if you're scared, buy half first" — does that actually work?

While running the simulations I stumbled on the fact that this old rule of thumb may really have legs. The report compares full lump sum, buying half, and splitting into thirds: in the scenario where a crash hits in year one, buying half dramatically lifts the win rate, while long-run performance barely suffers. It's essentially using half a year's gains as insurance — you can't predict when a crash will come, but that insurance lets you actually pull the trigger.

Can I still lose money over five years? Does holding longer help?

Yes. Over a 5-year horizon, there's roughly a 20–30% chance of ending up in the red. But stretching the holding period clearly lowers the loss rate — out to 15 years it drops into the single digits, and even the most stubborn stagnation scenario keeps falling. Time, more than anything, is the real answer to borrowing to invest — provided you're very, very patient.

What does the 'risk report' actually compute?

It's an advanced feature inside the loan-to-invest calculator: a Monte Carlo simulation that, across multiple market stress scenarios, runs 100,000 random return paths each, then tells you the lump-sum vs. DCA win rate, the probability of going "underwater" (assets below debt), how different phased-entry strategies compare, and how the loss rate converges as you stretch the holding period to 2× and 3× the loan term. It won't promise you'll profit — it gives you a probability, which is the right language for facing the unknown.

I'm not borrowing — I just have a lump sum on hand. Is this report still useful?

Yes. Set the loan rate to 0 and the report collapses into the purest question of all: should a lump sum go in all at once, or be spread out? Whether it's a year-end bonus, proceeds from selling a house, or an inheritance, you still face lump sum vs. DCA and sequence-of-returns risk — and the report's conclusions apply just the same.

About the Author

indigo.la.ringo

A software engineer chasing the slash-career dream. Was trying to figure out my relationship with the world — now being forced to figure out my relationship with AI. Lately, obsessed with figuring out the relationship between people and money. Either way, whatever answer I land on, it's fine.

Feedback

Thoughts or suggestions after reading? I'd love to hear them.