Rent vs. Buy Calculator Guide: Break-Even Year, Net Wealth, and Hidden Costs

I'm sure you've heard both sides of this argument:

"You're paying two or three thousand a month in rent — after a few years that's hundreds of thousands straight into your landlord's pocket. You're basically paying off someone else's mortgage!"

"The moment you buy, your down payment wipes out your savings. Then you're chained to a 30-year mortgage. What if you lose your job? There goes your quality of life..."

"Is it better to buy or rent?" is one of those questions that haunts a lot of people

Every time I tried to think it through

It felt so complicated that I'd give up after three minutes

But this could easily be the single biggest financial decision of your life

So why don't we actually sit down and do the math?

On one of those impulsive moments,

I started building the 👉 Rent vs Buy Calculator

to break this problem down into something manageable —

at least let's get the parts we can quantify out of the way

Part 1 — The Financial Blind Spots: What Are You Forgetting to Count?

To judge which option is really right for you,

you need to stretch the timeline out to 20–30 years

and factor in every additional cost

1. The "Hidden Costs" of Buying: It's Not Just the Mortgage

The costs most people forget about are the ones that pile up before and after moving in:

- One-time upfront costs: deed tax, stamp duty, notary fees, registration fees, agent commission (typically 1–2% of the purchase price), plus renovation and furnishing costs that can easily run into the tens or hundreds of thousands

- Ongoing holding costs: annual property tax and land value tax, monthly HOA/maintenance fees, and repair and upkeep costs as the building ages

- Interest expense: over a 30-year loan, the total interest you pay the bank often amounts to hundreds of thousands of dollars

Here's a rough breakdown for a typical home in the US priced at $500,000:

| Cost Category | Estimated % | Actual Amount ($500K) | Notes |

|---|---|---|---|

| One-time costs (new build) | ~7% | ~$35,000 | Closing costs $15K + renovation & appliances $20K |

| One-time costs (older home renovation) | ~14% | ~$70,000 | Closing costs $15K + full renovation & furniture $55K |

| Annual holding costs | ~2.0%/yr | ~$10,000/yr (≈$833/mo) | Property tax $7,500 + HOA/maintenance reserve $2,500 |

Just like buying a car —

once you factor in all the downstream costs

you realize the true entry cost is quite a bit higher than the sticker price

2. The "Opportunity Cost" of Renting: What Returns Are You Giving Up?

The biggest downside of renting is that the money you pay is just gone —

it doesn't convert into any asset

On top of that, many landlords resist reporting rental income

which means renters often can't access housing subsidies

Even if you try to claim them,

the landlord might find out and retaliate by kicking you out

So renters often end up at their landlord's mercy

But renters have one major advantage that buyers don't — financial flexibility

Buying a home requires a large down payment (say $100K)

If you choose to rent instead,

that $100K just sitting in a savings account or getting spent

gives you no asset appreciation compared to buying

But if you invest that $100K at a 6–8% annualized return in global index funds or high-dividend ETFs

could the compounding effect over decades

beat home price appreciation?

That opportunity cost of capital question

is something we'll revisit in the calculator section below

⚖️ Full Cost Comparison: Buying vs. Renting

| Item | Buying (acquiring an asset) | Renting (buying flexibility) |

|---|---|---|

| Upfront costs | Down payment (~20%), taxes, renovation & furnishings | Security deposit (typically 2 months), moving costs |

| Monthly fixed costs | Mortgage principal & interest, HOA fees | Monthly rent, HOA fees (if applicable) |

| Annual variable costs | Property tax, land tax, repairs | Usually none (landlord's responsibility) |

| Where the money goes | Principal builds equity; interest and taxes are sunk costs | Rent is a sunk cost; remaining capital is freely investable |

Part 2 — 3 Financial Metrics That Should Drive Your Decision

1. Price-to-Rent Ratio

This is the classic international metric for evaluating buy vs. rent, defined as:

- Above 20: Home prices are clearly elevated — renting is usually more cost-effective

- 15–20: Gray zone — depends on interest rates and your ability to invest

- Below 15: Home prices are relatively reasonable or rents are high — buying makes strong financial sense

The good news: in the US these benchmarks apply far more directly

because American homeowners already face significant property taxes (typically 1–2% of market value per year)

Those annual holding costs are the very reason the 15/20 thresholds were set where they are

That said, the ratio varies dramatically depending on where you live:

- High-cost coastal metros (San Francisco, New York, Seattle): 25–40+

- Mid-tier Sun Belt cities (Austin, Denver, Nashville): 18–22

- Affordable Midwest and Southern cities (Cleveland, Indianapolis, Memphis): 8–14

For our baseline scenario — a $500,000 home at $2,200/month in rent:

$500,000 ÷ ($2,200 × 12) = $500,000 ÷ $26,400 = 18.9 — right in the gray zone

This puts the "buy vs. rent" question squarely in "it depends" territory

where mortgage rate and investment discipline become the decisive factors

2. Expected Stock Market Returns vs. Expected Home Price Appreciation

If you struggle with investing discipline and tend to spend freely,

the "forced savings" effect of owning a home can be genuinely helpful

On the other hand,

if you can consistently achieve 6–8% investment returns,

renting + investing may build more wealth over the long run

3. Your 5–10 Year Residency Plans

The transaction costs of selling a home in the short term are high (heavy taxes + agent fees)

If there's any chance you might change jobs, move abroad, or get married in the near term,

renting is usually the better choice

General guidance: if you don't plan to stay in one place for at least 5 years,

renting should be your default

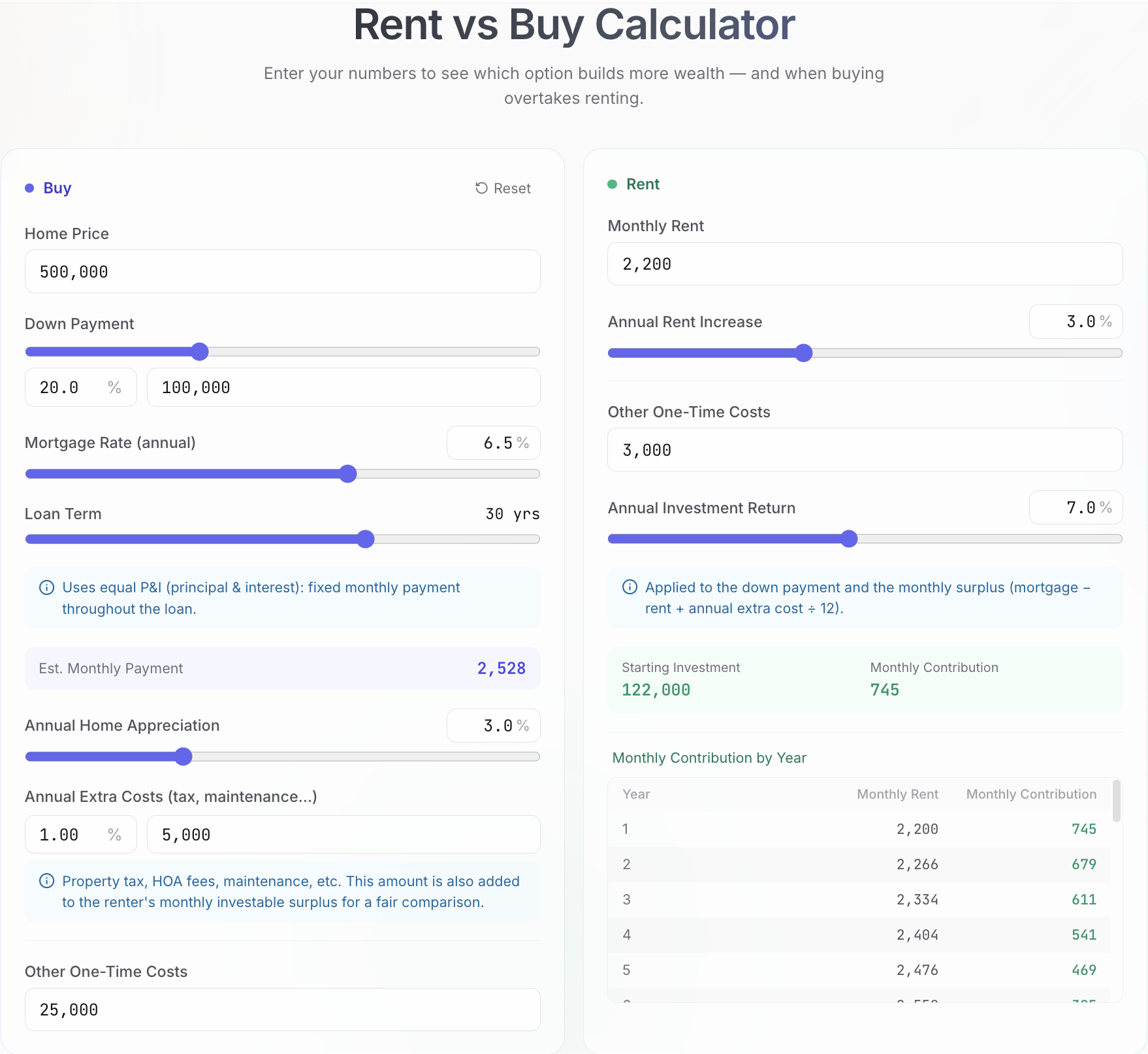

Part 3 — Run the Numbers with the Rent vs. Buy Calculator

Let's simulate a scenario common among young professionals in a mid-tier US metro:

📝 Assumptions (Numbers are illustrative — plug in your own situation)

- Alex (age 30): has $125,000 in savings

- Target home: 2-bedroom condo, total price $500,000

Scenario A (Buy): $100K down (20%), $400K loan (80%), 30-year at 6.5% → monthly payment $2,528$5,000/yr)

$25K upfront for closing costs + furnishings; projected home appreciation 3%/yr; annual holding costs (property tax, HOA, repairs) 1.0% (

Scenario B (Rent): comparable unit at $2,200/month, rising 3%/yr; $3K upfront for moving + small appliances

All $122,000 in remaining savings + the dynamic monthly cash-flow difference invested into an ETF at 7% annualized

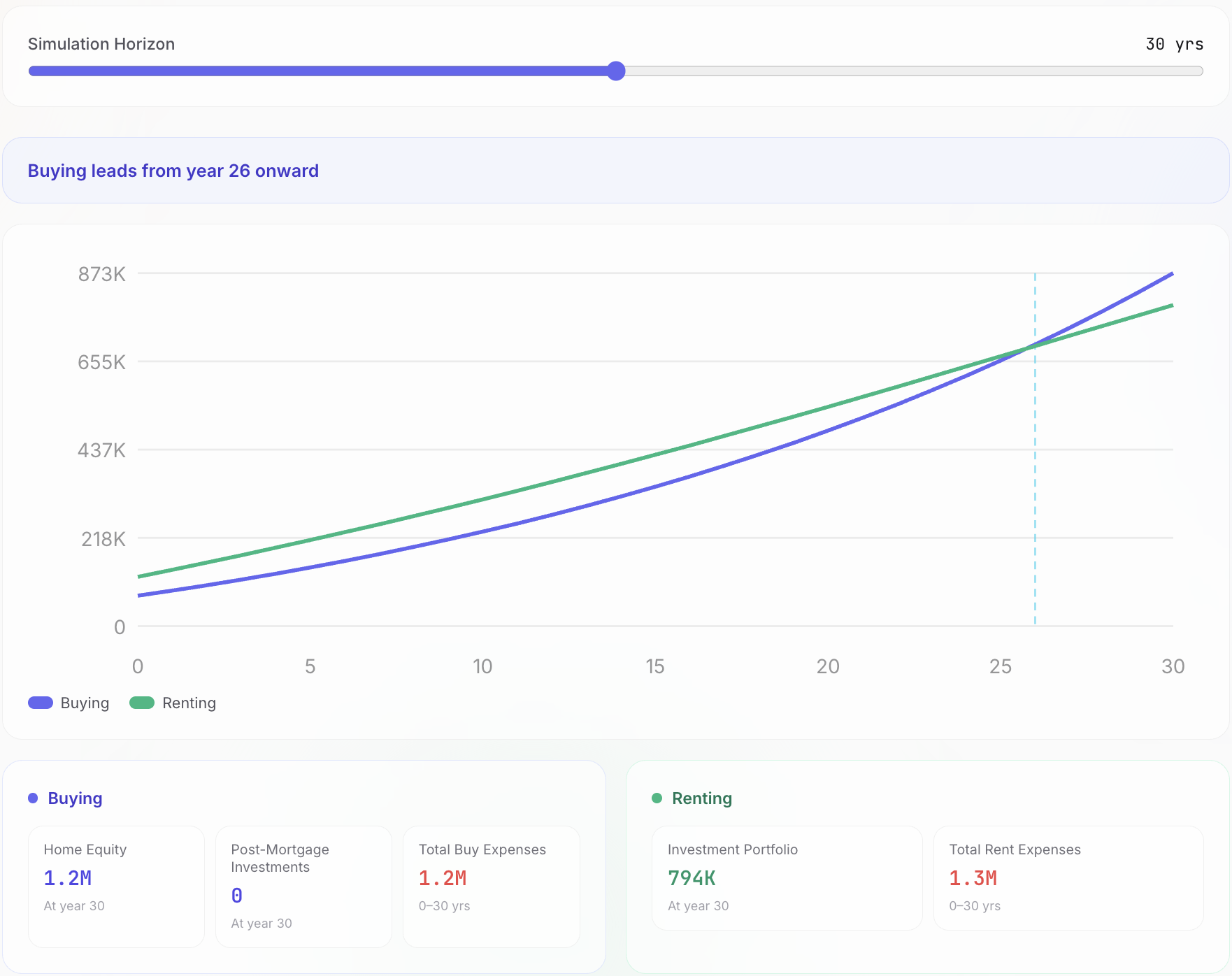

💡 Key Findings

- First ~25 years: Renting + investing leads — the renter's portfolio (starting at $122K) outgrows the buyer's slowly-building equity, because the 6.5% mortgage front-loads interest in the early years

- ~Year 26: The crossover — as the mortgage gets paid down and equity compounds, buying's net worth finally overtakes

- Year 30: Buying edges ahead (~$873K vs ~$794K), but the margin is thin — at a 6.5% rate the verdict is close and flips easily when you nudge appreciation, rent, or the holding-cost assumption

Part 4 — Try the Calculator with Your Own Numbers

Instead of looking at someone else's scenario, run your own!

- Enter your buying parameters (home price, down payment, interest rate, loan term)

- Enter your renting and investing parameters (monthly rent, expected return)

- See the 30-year net worth comparison and the golden crossover year at a glance

Give it a spin: 👉 Rent vs Buy Calculator

Wrap-Up: No Right Answer — Only the Best Answer for You

Buying or renting

has never had a universal right or wrong

Buying isn't just a place to live — it's forced savings, and your final asset is a physical property

- You prioritize stability

- You're not great at investing on your own

- You have a strong desire to own and plan to stay in one place for 10+ years

→ Buying may be the right choice for you

Renting means paying for flexibility — your final net worth depends entirely on whether you actually invest the down payment you kept

- You prioritize life flexibility

- You have investment discipline

- Your future location is uncertain

→ Renting + investing is the right choice

I hope this calculator helps you cut through the anxiety and confusion

and make the decision that fits your current stage of life.

This article is for financial education purposes only. Simulation data is based on hypothetical scenarios and does not constitute investment or home-buying advice. Real estate markets are influenced by macroeconomic conditions, interest rates, policy changes, and many other factors — actual results may differ significantly from simulations. Please make decisions based on your personal financial situation, risk tolerance, and professional advice.

References & Further Reading

Frequently asked questions

What is the Price-to-Rent Ratio?

The Price-to-Rent Ratio = Home Price ÷ (Monthly Rent × 12). Above 20 means renting is usually more cost-effective; 15–20 is a gray zone; below 15 means buying makes strong financial sense. In high-cost coastal metros like San Francisco the ratio typically runs 25–40+, while affordable Midwest cities often see 8–14.

What is the break-even year in rent vs. buy?

The break-even year is the point at which the homeowner's net wealth equals or exceeds the equivalent renter's net wealth — where the renter invested their down payment and monthly savings difference in a diversified portfolio. In a $500K home at a 6.5% mortgage rate with $2,200 rent, the renter leads for the first ~25 years and buying only overtakes around Year 26 — a high mortgage rate pushes the crossover late.

Should I rent or buy right now?

It depends on three factors: your Price-to-Rent Ratio, your 5–10 year residency plans, and your investment discipline. If you plan to stay fewer than 5 years, renting is usually better due to high transaction costs. If your local PTR is above 20, renting is typically more cost-effective. If you lack investment discipline, the forced savings of homeownership has real value.

What hidden costs do buyers forget?

Buyers typically undercount: deed tax, agent commission (1–2% of purchase price), renovation and furnishing costs, annual property tax (1–2% of value in the US), HOA/maintenance fees, and repair reserves. For a $500K home, one-time costs can reach $35,000–$70,000 and annual holding costs around $10,000/year.

About the Author

indigo.la.ringo

A software engineer chasing the slash-career dream. Was trying to figure out my relationship with the world — now being forced to figure out my relationship with AI. Lately, obsessed with figuring out the relationship between people and money. Either way, whatever answer I land on, it's fine.

Feedback

Thoughts or suggestions after reading? I'd love to hear them.