Borrowing to Invest: Reckless Gamble or Rational Choice?

I've been seeing the news lately

We've apparently entered an era of second, third, even fourth loans all under one roof

Plenty of people take out personal loans to play the property and stock markets

and get slapped with all sorts of high-risk labels

So is this the legend of the teenage stock god

or the product of a rational choice?

"Fear comes from the unknown"

Rather than blindly following the crowd, it's better to do your own research

This article is part of what I've learned from my own digging

and along the way I built a little tool to compare this whole "loan-funded stock investing" idea

I trust you'll agree that in this day and age, investing is no longer an elective

so let's get to know what borrowing really means, together

What is borrowing to invest, really?

At its core, borrowing to invest (which is really a form of leverage) comes down to a single sentence:

You expect your "investment return" to be higher than your "borrowing cost (interest)" over the long run

In other words, it's the spread between your investment return and your loan interest.

As long as that spread is positive

you can use cheap interest

to buy the "time" of someone else's money

and put that capital to work for you sooner

This is also part of how many financial institutions make money:

they obtain funds at a lower cost of capital

then deploy them into higher-returning assets to earn the spread.

The problem is

in real life no one can guarantee

that this spread will always exist

So why do people still flock to it?

And what kind of risks are hidden behind it?

We'll savor them one by one in a moment

But before that

we need to be clear about what we're comparing against

The control group: comparing against "dollar-cost averaging"

After all, the whole premise of borrowing to invest is that you assume some asset's

positive returns will outweigh the interest

So what we should really compare is:

investing the same amount each month

but without borrowing

putting that money into the same asset via dollar-cost averaging

That is, Lump Sum Investment (LSI)

vs.

Dollar-Cost Averaging (DCA)

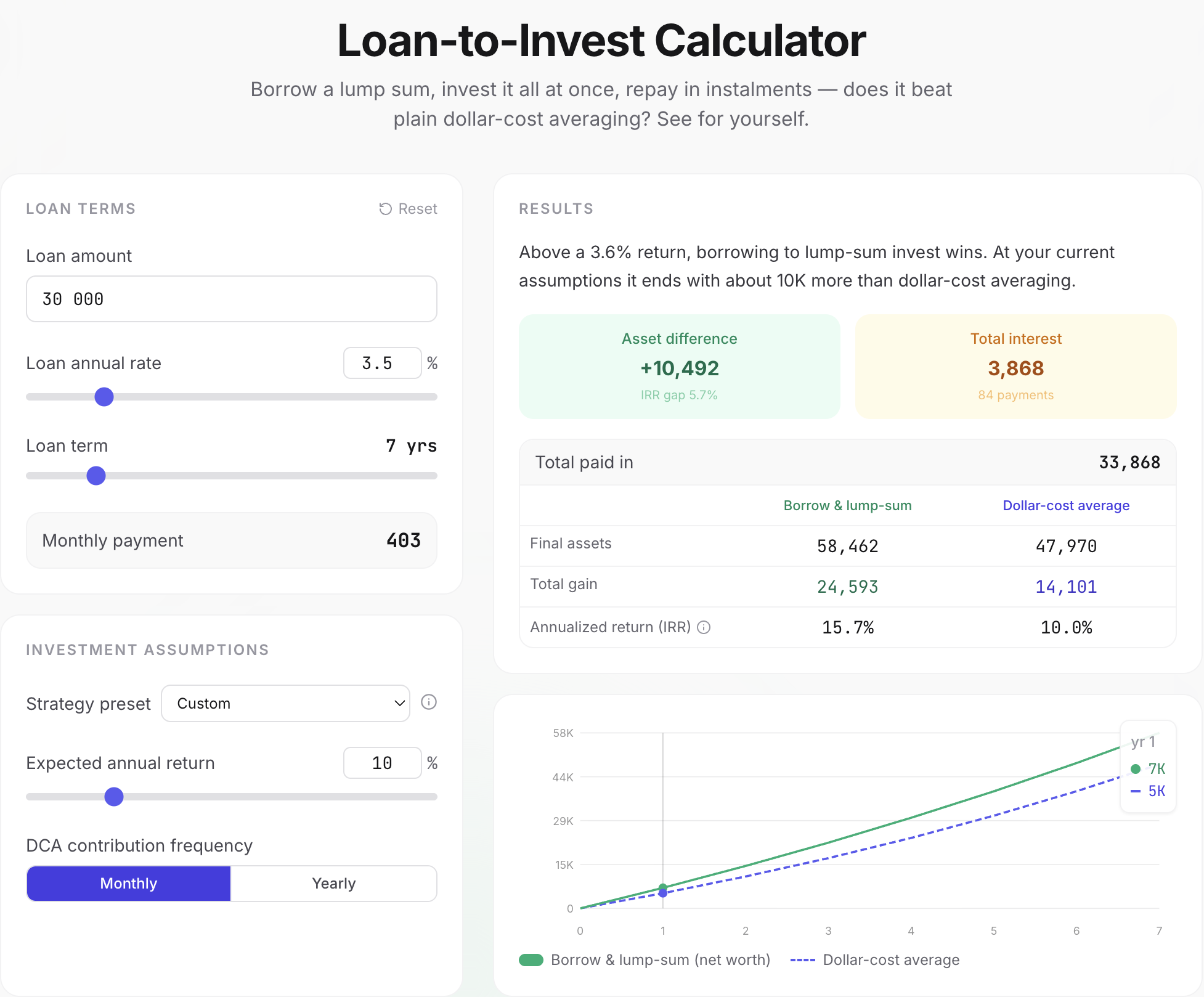

This is exactly what the little tool 👉 Loan-to-Invest Calculator is designed for:

- Loan-funded lump sum: borrow a chunk of money, invest it all into the index immediately, then repay principal + interest each month

- Dollar-cost averaging: don't borrow; take the same amount as the monthly repayment and invest it into the same index, bit by bit

Both strategies put out exactly the same cash each month

The only difference is that the loan-funded lump sum lets the capital "participate in the market earlier"

and the price for that is the interest

Let's actually run the numbers: a 5-year, $30,000 personal loan

Say you have a $30,000 personal loan

at 3.5% interest over 5 years

which works out to a monthly repayment of about $546

For the investment, let's pick SPY (1996–2025, with an annualized return of roughly 10.2%–10.8% over the past 30 years)

Scenario A (loan-funded lump sum): borrow $30,000 and invest it immediately into SPY at a 10% annual return, then repay $546 each month

Scenario B (dollar-cost averaging): don't borrow; invest $546 into the same ETF each month via DCA

| Item | Loan-funded lump sum (LSI) | Dollar-cost averaging (DCA) |

|---|---|---|

| Total assets at maturity | ~$48,315 | ~$41,783 |

| Total interest paid | ~$2,745 | ~$0 |

| Net investment return | ~$15,570 | ~$9,038 |

- Monthly cash out of pocket: ~$546

- Total invested over 5 years: ~$32,745

- Asset difference: the loan-funded lump sum beats dollar-cost averaging by about $6,532

Putting out the same $546 every month

the borrower — because the full $30,000 has been compounding in the market since day one —

ends up with nearly $6,500 more after 5 years

and even after subtracting the ~$2,745 in total interest costs

they're still well ahead

The calculator spells it out too: above a break-even return of about 3.6%, the loan-funded lump sum comes out ahead

In an idealized model with a fixed return rate higher than the borrowing cost

leverage delivers a positive expected value

that is, the gains from getting capital into the market earlier

have a chance of exceeding the borrowing cost

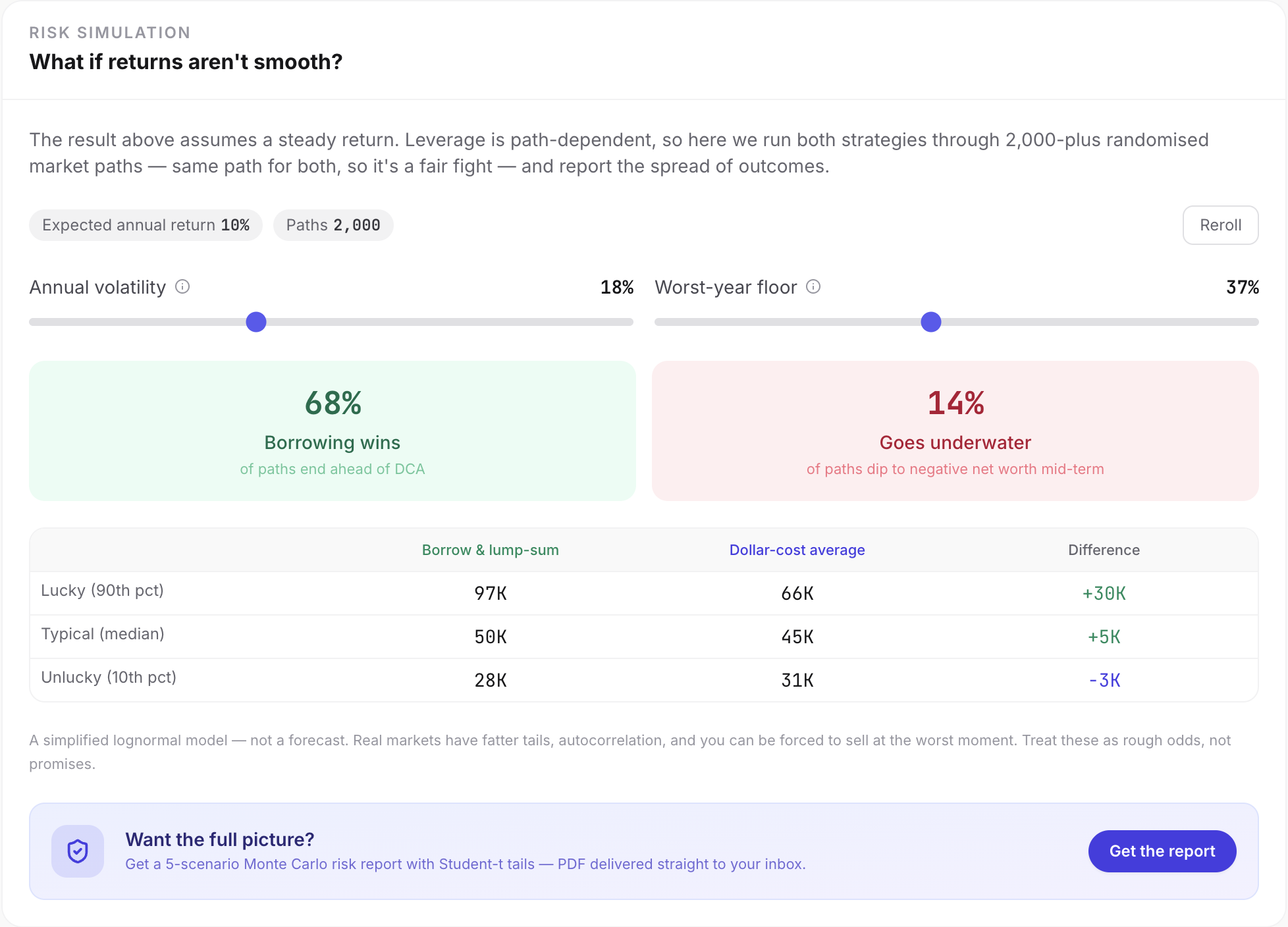

But what about reality?

Does "wins in theory" = "you'll definitely win"?

So far it looks like

as long as the return rate stays comfortably above the loan rate

borrowing to invest is a sure win, right?

But just because Gojo Satoru says he'll win, does he really win?

If the world's return rate really were a smooth, upward-sloping line

then yes, it would be

And in that case personal loan rates should be just as high as stock returns

after all, who wouldn't grab free money?

But the real market is not a steadily rising slope

and the most deadly thing of all is sequence-of-returns risk

Sequence-of-returns risk

Put simply

because a lump sum gets no new money added along the way

if you hit a drop-then-rise scenario

dollar-cost averaging has a chance to buy in at cheaper prices

so it can ultimately deliver a bigger return than the lump sum

Suppose LSI invests a total of 300

and DCA invests 150 across two rounds

| Scenario | Price path | LSI final assets | DCA final assets |

|---|---|---|---|

| Rise then fall | 100 → 240 → 120 | 360 | 255 |

| Fall then rise | 100 → 50 → 120 | 360 | 540 |

The reason borrowing to invest cares so much about sequence-of-returns risk

is that the borrowed capital is all in the market from day one

so if the market crashes right at the start

the largest principal is immediately exposed to risk

whereas dollar-cost averaging can keep accumulating more shares during the downturn

That's why in certain "fall then rise" scenarios

DCA's outcome can even beat LSI's

The thing borrowing to invest fears most is a big crash in the first year or two of the loan

because the principal is at its largest early on

and once the share price gets cut in half

even if the market recovers later

the power of compounding takes a heavy hit

That's exactly why I added a simulation feature in the second part

The investment is again SPY (1996–2025, with an annualized volatility of roughly 16%–18% over the past 30 years)

The investment is again SPY (1996–2025, with an annualized volatility of roughly 16%–18% over the past 30 years)

Assuming a 10% annual return and 15% volatility

with a maximum single-year drawdown of 37% (the financial-crisis-level decline)

running a Monte Carlo simulation 2,000 times

we find that

under these conditions, the loan-funded lump sum wins in about 73% of cases

In addition, in about 4% of the simulated scenarios

the asset's market value at some point fell below the remaining loan balance

meaning there may be a stretch where selling all your stock still isn't enough to repay the debt

If you can't stomach the volatility and cut your losses at that moment

you may miss out on the rich rewards that come afterward

And even if you're lucky enough to avoid that situation

once your cash flow can't cover the repayment on time

you may be forced to sell stock anyway

These risks all have to be taken into account

But look closely

sequence-of-returns risk might cost you some upside

yet as long as you can firmly hold for the long term

the gap in returns isn't actually that large

Over the long run, as long as the investment return keeps exceeding the borrowing cost

the loan-funded lump sum still has the higher expected value

So is borrowing to invest right for you or not?

An investing mentor I really admire (Brother Daren) once said something

if you're just asking this simple yes/no question

it means you're not ready yet

the answer is NOOOOOO

I've broken it down into a few questions myself

hoping to help everyone get clarity on their own situation

People who can seriously consider it

- The money you borrow is low-interest and long-term, like a home loan after a top-up refinance, or a low-rate personal loan

- You have stable and predictable income, the monthly payment is a small share of it, and a sudden loss of salary won't leave you unable to repay

- You keep an emergency fund that is separate from this investment

- You have high risk tolerance and are a firm long-term investor

People who really shouldn't touch it

- Those who throw in their emergency fund, or even living expenses, along with everything else

- Those with unstable income, or who'd hit a cash crunch the moment one payment is missed

- Those who can't sleep at the sight of a paper loss and can't resist cutting their losses at the very bottom

- Those who only read my one-sided notes without doing any other homework

My next step

If you're currently weighing the risks and opportunities of borrowing to invest

here are a few things worth thinking through before you act:

- Take stock of your own cash flow

- Examine your own risk tolerance

- Prepare a sufficient emergency fund

- Evaluate the asset you're investing in

- Think through how you'd respond in different scenarios

What truly decides success or failure

is often not how high the investment return is

but whether you can stay in the market

even through the worst-case scenario

This calculator and article are for educational reference only. They use a deterministic calculation with a single fixed return rate, and do not account for market volatility, sequence-of-returns risk, taxes, or personal circumstances. Borrowing to invest is a leveraged activity that magnifies both gains and losses; for actual decisions, please consult a qualified financial advisor and act within your means.

References and further reading

Frequently asked questions

What's the core principle of borrowing to invest?

It comes down to one idea: you expect your long-term investment return to exceed the cost of borrowing (the interest). That gap is the spread. As long as the spread is positive, you're using cheap interest to buy time for your capital — letting it compound in the market earlier. The catch is that no one can guarantee the spread holds, and that's exactly where the risk lives.

What is the break-even return rate?

It's the annualized investment return at which a loan-funded lump sum and dollar-cost averaging end up with the same final assets — roughly a touch above your loan rate. For a $30,000 personal loan at 3.5% over 5 years, the break-even return lands around 3.6%. As long as your long-run return stays comfortably above that line, the loan-funded lump sum has the higher expected value.

Does a loan-funded lump sum always beat dollar-cost averaging?

No. The biggest variable is sequence-of-returns risk — borrowed money is fully invested on day one, so a crash in the first year or two hits the largest principal immediately, while DCA keeps buying cheaper shares during the dip. In a Monte Carlo simulation (10% return, 18% volatility, 37% worst-year drawdown, 2,000 runs), the loan-funded lump sum wins about 73% of the time — but in roughly 14% of scenarios the portfolio value dropped below the remaining loan balance at some point, i.e. underwater.

Who should and shouldn't borrow to invest?

Better suited: those borrowing at a low rate over a long term (e.g. a home-equity top-up), with stable, predictable income where the monthly payment is a small share of it, a separate emergency fund untouched by the investment, and the discipline to hold for the long run. Should avoid: anyone pouring in their emergency fund or living expenses, with unstable income, who can't sleep through paper losses and would panic-sell at the bottom, or who acts on a single article without doing their own homework.

About the Author

indigo.la.ringo

A software engineer chasing the slash-career dream. Was trying to figure out my relationship with the world — now being forced to figure out my relationship with AI. Lately, obsessed with figuring out the relationship between people and money. Either way, whatever answer I land on, it's fine.

Feedback

Thoughts or suggestions after reading? I'd love to hear them.